Executive Summary

This is Enbridge’s first report addressing recommendations made by the TCFD. It discusses our evolving approach to integrating climate risks and opportunities into our governance structure and strategic planning, and how we identify and mitigate risks. It outlines the role of our Board and executive leaders in ensuring that climate considerations are part of our decision-making frameworks for risk management, business planning and performance evaluation.

Our annual sustainability reporting—which commenced in 2001—has previously addressed many climate-related issues. This report provides more in-depth discussion about how we view risks and opportunities for our business within the context of evolving energy systems both in North America and globally. Future TCFD-related updates will appear in our annual Sustainability Report.

In this report, we apply two International Energy Agency scenarios—the New Policies Scenario (NPS) and the Sustainable Development Scenario (SDS)—to test the resilience of our strategy and energy infrastructure. We apply the scenarios to our three core businesses—liquids pipelines (LP), gas transmission and midstream (GTM), and gas distribution and storage (GDS)—and to our renewable energy investments. The NPS forms our base-case scenario and we use the SDS as a lower-probability, higher-consequence scenario to stress test our asset base and strategy.

Our analysis indicates that our core assets are resilient under both the NPS and the SDS. Under the NPS, supply and demand fundamentals suggest our assets will be used and useful through 2040 and beyond with significant opportunity for growth within each business unit. Under the SDS, there is still a strong utilization of our assets but there is also a higher volume and cash flow risk to Enbridge in the longer run—particularly in our LP business. Yet, in both scenarios our risk is mitigated by strategically located assets which connect key supply basins with demand-pull markets both within North America and internationally. Our assets are particularly valuable given the North American competitive advantage for supplying oil and gas to the world and the difficulty inherent in building new oil and gas infrastructure in North America.

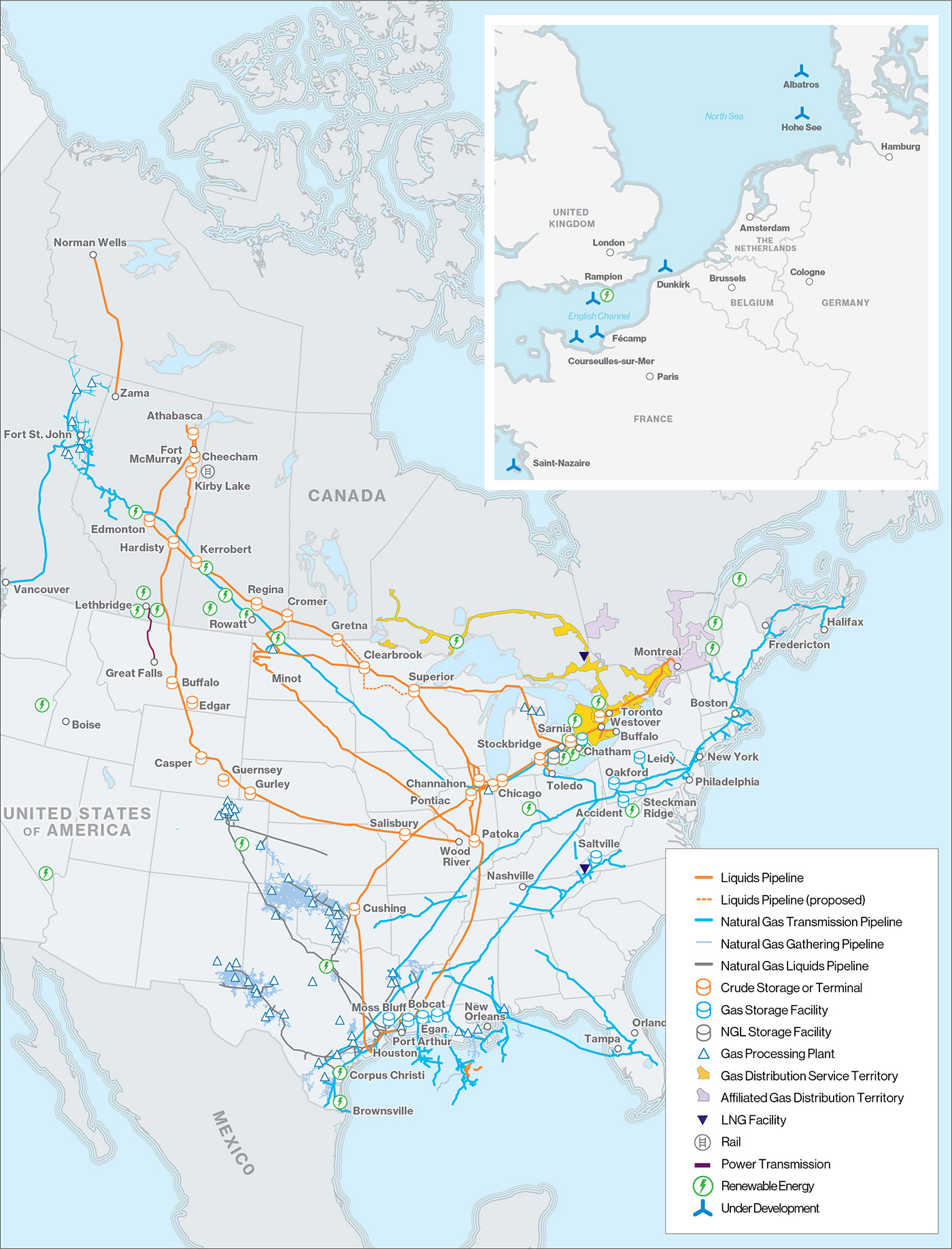

Our business model further mitigates risk with low-risk commercial structures, low-cost delivery to the best industrial, commercial and consumer markets, long-term contracts, and strong risk-adjusted returns. That said, if the SDS scenario emerges, we are positioned to transition our business more rapidly to reflect evolving energy supply and demand fundamentals. In recent years, we have become more resilient by diversifying our assets to reflect an evolving global energy mix. We have taken a much bigger position in lower-emission natural gas and we continue to pursue further investment in renewable energy projects. We currently have the capacity— either operating or under construction—to generate more than 1,700 MW (net) of zero-emission energy. We have developed a joint venture with the Canada Pension Plan Investment Board (CPPIB) to grow our existing European offshore wind portfolio.

We are also encouraging and applying clean technology across our entire energy system. Each of our businesses has a role to play in meeting demand while reducing emissions. We believe that applying data analytics to our businesses will improve the efficiency of our operations while achieving economic and climate benefits. Our LP business is using Drag Reducing Agent—a product injected into crude oil to reduce pipeline fluid friction—to allow certain pump stations to be bypassed, thus reducing total electricity consumption. Our GTM business unit has been—and continues to be—instrumental in supporting the switch from coal to natural gas and renewables in the U.S. Our GDS business is deploying technologies for producing pipelinequality natural gas with a lower-carbon footprint, including renewable natural gas (RNG) and power-to-gas (P2G) technology, which uses renewable energy to produce hydrogen. We are providing our GDS customers with access to better products, services and programs for cost and emissions reduction through energy efficiency and Demand Side Management (DSM).

The metrics and targets section of this report shows that our efforts are paying off. At an enterprise level, we have set and met two “top-down” GHG reduction targets. The data demonstrates that we've made some progress reducing emissions on an intensity basis but we have more work to do. We are challenging each of our business units to develop “bottom-up” targets for reducing direct and indirect (Scope 1 and Scope 2) GHG emissions (see glossary on Page 27 for definitions). We will also be exploring new and modified metrics to help ensure effective performance and reporting of GHG emissions associated with our business. These mechanisms will help to ensure that our strategy and asset base remain resilient over the long term.